Marrying Someone With Debt! Let’s See How Does Marriage Affect Debt?

- What happens when you marry someone with debt or bad credit?

- Does his or her debt become yours as well?

- Are you responsible for your spouse’s debt after marriage?

Well, there are many misconceptions about marriage and debt, so let’s check out the myths and facts related to this question.

Read: My Credit Score: Why Good or Bad Credit Scores Matter

When you find a partner whom you love and want to spend the rest of your life with, but the only hitch is that he/she has debt, what happens to your financial situation?

Money can be a major issue on which couples fight and separate, so it is important to know all aspects of debt and marriage before you tie the knot!

Is Your Partner’s Debt Your Debt Too?

Do you inherit your spouse’s debt when you get married? In most of the states, a person is not legally liable for the debt of their spouse incurred before marriage. However, the state you are living in could change this.

- In case of the common law states, you will responsible for paying off the debt if you open a joint account or have a shared credit card. Once you have signed up for a shared bank account, the liability also becomes shared, no matter when it was incurred.

- As a married couple, if you open a joint account or if you have a shared credit card, then you both are responsible for paying back debts.

- In case of community property states, you have to share debts taken after marriage but are not liable for debts that are incurred before marriage by your spouse.

The laws differ in the nine community property states of America where one is not responsible for a spouse’s debt that has been incurred before marriage.

Credit Scores: When You Marry Someone With Debts

How will your marriage and your spouse’s debt affect your credit score? Let’s find out what happens when you change your name on your credit report.

- The good news is that your credit scores will not be affected by your spouse’s debts. You will continue to have your separate credit report, score and history and your report will not reflect your spouse’s negative information.

- Even if you change your name to your spouse’s name, your credit history will not be changed or affected, as the information is connected with your individual social security number.

However, if you are a joint account holder for the bank account in which the loan has been taken and, you will also share debt responsibility.

Change of Last Name

Let’s see how a change of last name can affect your credit history and debt position when marrying someone with debt.

- Credit systems allow men and women to change their last names, thereby allowing several last names for a single individual’s credit report.

- When you get married and change your last name, the new name gets linked with your original credit report once you notify creditors of your new name and the creditor updates it. The old name will also continue to remain a part of the credit history to make it complete and accurate.

- If you keep your credit account in your name alone, you will not be accountable for any debt incurred by your partner before marriage.

Remember: Do not add your name to your partner’s debt!

If you have merged your accounts, both of you are jointly responsible for any debt incurred in the the joint credit accounts. A missed payment will be reported in both the spouses’ records.

Joint Credit Loans

- If you incur a joint debt with your spouse, it will impact on your score. For instance, if you share a house mortgage and if your partner does not make the payment in time, both your scores could get impacted negatively.

- If you apply for a loan jointly and if your spouse has a low credit score due to unpaid debts, you may also not qualify or may have to pay a higher interest rate due to your spouse’s low credit score and debt.

Also See: 11 Vital Things to Teach Your Child About Using Credit Cards

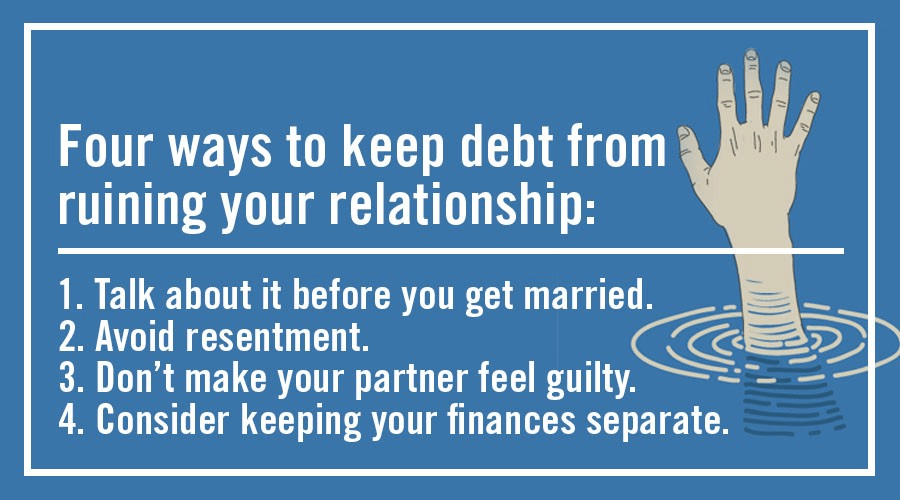

Precautions to Take

Honesty is great in a marriage but it is also wise to take a few precautions in case of financial matters and when you marry someone with debt.

- Do not add your name to your spouse’s debt, though you might consider yourself as a team, because if you do so, you are also liable for paying off the debt. If the debt belongs to the spouse alone on paper, you are not liable for payment.

- If you put your credit cards and loans in your name alone and not jointly, you stand a better chance of not being impacted. This is because if your spouse had an earlier debt, his/her credit scores would be lowered and this could impact a joint loan request.

- If you have a prenuptial agreement defining how the debts can be allocated, along with repayment of debts, you will not have to suffer the consequences of a pre marriage debt of your spouse.

Must Read: Benefits of Reverse Mortgage for Senior Citizens

Wrap Up – Marrying Someone With Debt

Imagine this scenario! You have spent an entire lifetime of paying off all debts and making good savings. When you marry the person you love, your partner has not done so and is in quite a bit of debt maybe!

Of course, marriage is for better or for worse but it is not fair that all your diligence, hard work and savings should go waste and you incur your partner’s debt! Check out ways of protecting your wealth even after marrying someone with debt.

The bottom line is that premarital debt of your spouse will never become a joint debt. But once you are married, any debt racked up by your spouse could also impact you, depending on where you live, community property states or common law states.

Legally, any pre existing debt is the responsibility of the person incurring it and will only affect the credit score of that person.

Unusual Ways to Make Extra Money Doing Odd Jobs

Unusual Ways to Make Extra Money Doing Odd Jobs 10 Household Items You Can Sell Today for Quick Cash

10 Household Items You Can Sell Today for Quick Cash